What Maria did to get

thousands of more dollars

for her total-loss vehicle

than the valuation amount

in the CCC market valuation report.

Maria’s total-loss claim

was a first-party claim.

She was dealing with

her own automobile insurance company.

Maria filed her first-party total-loss claim

soon after her 2018, 5‑door,

Grand Touring Mazda3 was totaled.

Maria received a “market valuation report”

from her insurance company.

CCC Information Services

a.k.a. CCC Intelligent Solutions

had prepared the report.

Maria was distressed at how low

the report’s valuation was.

The CCC market valuation report

valued Maria’s totaled vehicle

at $17,467 (sales tax not included).

The valuation was less

than the balance of her car loan.

If there was nothing that she could do

and she had to accept this valuation, then

she would have to keep making payments

on an automobile that no longer existed.

I told Maria that,

when my automobile was totaled,

I did not accept

the insurance company’s valuation.

I told her what I did to challenge it.

I told Maria that CCC

had generated a market valuation report

for my total‑loss vehicle for Travelers.

The CCC market valuation report

had lots of omissions, errors,

and other problems.

A careful reading

of the CCC market valuation report

led me to suspect

that Travelers and CCC

had conspired to cheat me

out of a fair valuation

of my total-loss vehicle.

I told Maria that, to start with,

she might want to check

the CCC market valuation report

for her totaled vehicle

for omissions and errors

in the description of her total‑loss vehicle.

Thus alerted, Maria examined

the CCC market valuation report

on her car.

Maria found that

the CCC market valuation report

left out her car’s

communications system,

intelligent cruise‑control system,

lane‑departure warning system,

lane keep assist, metallic paint,

wheel‑lock anti‑theft tire‑protection system,

heated steering wheel, automatic braking,

Homelink universal garage door opener,

and auto‑dim rearview mirror.

Maria sent the claims agent an email

in which she notified the claims agent

of these omissions.

The claims agent had CCC

re‑run the valuation

with the omitted options included.

CCC came back

with a revised market valuation report.

The revised CCC market valuation report

added a measly $450

to the value

of Maria’s total‑loss vehicle.

The “revised” CCC market valuation report

valued her total‑loss vehicle

at $17,917, a valuation increase of only 3%.

Maria then asked me to look

at the CCC market valuation report

with her.

Before we did that, I suggested

that we find out what a fair valuation

of her total‑loss vehicle would be.

Like most other state insurance

commissioners, the New Jersey

Commissioner of Banking and Insurance

allowed insurance companies

to use NADA Guides retail values

to value total‑loss vehicles.

(NADA Guides is now J.D. Power.)

To get an exact NADA Guides valuation,

we needed detailed information

on her Mazda3.

To make our task easier,

we wanted to get a digital copy

of her total‑loss vehicle’s

Monroney Label window sticker.

To get a digital copy,

Maria went to the website

www.monroneylabels.com,

entered the Mazda3’s VIN number,

paid the $7.99 fee (now $9.99),

and had a PDF of the Monroney Label

instantly emailed to herself.

With the Monroney‑Label in hand,

to get a fair retail valuation

of Maria’s Mazda3,

we went to www.nadaguides.com.

At www.nadaguides.com,

we stepped through

the vehicle‑selection dialog:

-

manufacturer,

-

model year,

-

model,

-

trim level,

-

ZIP Code,

-

mileage,

-

and major options.

CCC’s initial valuation was $17,467.

CCC’s revised valuation was $17,917.

NADA Guides gave us

a retail price with options of $21,625

(sales tax not included).

$21,625 - $17,467 = $4,158.

$21,625 - $17,917 = $3,708.

The NADA Guides value was $4,158 more

than CCC’s initial valuation.

It was $3,708 more

than CCC’s revised valuation.

“Why?” we wondered.

We examined

the CCC market valuation report

for Maria’s totaled vehicle.

We focused on the methodology

that CCC used to value her vehicle.

When we realized

how CCC had concocted

such a low valuation,

our faces contorted

like we had just sucked lemons.

Our heads swiveled to face one another.

Our eyeballs rolled back into our heads!

Based on what we discovered,

Maria wrote a letter

to her insurance company.

She wrote a covering email.

She attached the letter to the email.

She attached to the email a PDF

of the NADA Guides valuation report

that we generated.

She attached to the email a PDF

of the Monroney Label window sticker

that she got from monroneylabels.com.

Maria sent the email and attachments

to the claims agent.

Here’s what the letter

(slightly redacted and clarified)

that Maria sent to the claims agent said:

Dear REDACTED,

Thank you ever so much for your gracious help

with my total‑loss claim.

I especially appreciate your offering

to work with me to come up with

a loss‑vehicle valuation that is fairer

than the one that CCC submitted to you.

After the experience that a close friend of mine

had with CCC, I cannot help but be suspicious

of any valuation that CCC provides.

A drunk driver passed out, crashed into

and destroyed a parked vehicle

that belonged to my friend.

Travelers was the insurer

for the drunk driver’s vehicle.

Travelers had CCC perform the valuation

of my friend’s total‑loss vehicle.

My friend found CCC’s valuation

to be blatantly fraudulent.

He exercised his right of recourse.

Travelers refused give my friend

a fair valuation of his total-loss vehicle.

My friend sued.

He won an award that was several times

the amount of CCC’s initial valuation

of his total‑loss vehicle.

Similarly, CCC appears to be

playing fast and loose

with the valuation of my total‑loss vehicle.

None of the three “comps”

that CCC used to value my total-loss vehicle

satisfy the legal definition

of substantially similar vehicles.

Also, the nine other “comps”

that CCC lists on its valuation document

do not satisfy the legal definition

of substantially similar vehicles.

According to the New Jersey

administrative code that governs

automobile physical damage claims:

“ ‘Substantially similar vehicle’ means

a vehicle of the same make, model, year

and condition, including all major options

of the insured vehicle. Mileage

must not exceed that of the insured vehicle

by more than 4,000 miles. Mileage differences

of more than 4,000 miles may,

at the option of the insured,

be exchanged for the presence or absence

of options or a cash adjustment.”

My total‑loss vehicle had 30,440 miles

on the odometer.

CCC’s three “comp” vehicles

have mileages of 4,020 miles; 5,186 miles; and 7,706 miles—

for an average mileage of 5,637 miles.

30,440 miles minus 5,637 miles

equals 24,803 miles.

A difference of 24,803 miles is

more than six times the legal limit

for a substantially similar vehicle.

Hence, CCC’s valuation

appears to be intentionally inconsistent

with the substantially similar requirements

of New Jersey state law.

In its bogus valuation, CCC

appears to use the mileage differences

to reduce the Base Vehicle Value in two ways:

-

Under Vehicle Allowances,

CCC deducts $892

with the questionable claim

that my total‑loss vehicle had more miles

than the average vehicle. -

From the average value

of its three “comp” vehicles,

CCC deducts $3,186.

CCC does not make it possible for claimants

to mathematically analyze their valuations.

They hide their opaque manipulations

under the explanation:

“Finally, the Base Vehicle Value is

the weighted average of the adjusted values

of the comparable vehicles

based on the following factors:

-

Source of the data (such as inspected versus advertised)

-

Similarity

(such as equipment, mileage, and year) -

Proximity to the loss vehicle’s

primary garage location -

Recency of information”

Accordingly, I cannot figure out whether,

by using their non‑comp “comps,”

CCC is attempting to penalize me $3,186

or [($3,186 + $892) = $4,087].

Going by the $3,186 average deduction

for the “comps,” it appears

that CCC is attempting to penalize me

for the 24,803 average difference in mileages

at the rate of $0.1285 per mile.

Since the maximum difference in mileages

that the law allows without the consent

of the claimant is 4,000 miles;

the maximum penalty for mileage difference

appears to be $514.

Hence, to bring CCC’s valuations

into closer compliance with the law

would mean adding back

to the average comp value

at least $3,186 - $514 = $2,672.

CCC lists nine other “comp” vehicles

in their bogus valuation document.

Those vehicles have odometer readings of:

3,359 miles; 3,019 miles; 4,237 miles;

6,965 miles; 5,035 miles; 7,370 miles;

5,439 miles; 2,254 miles; and 4,031 miles.

Hence, the difference in mileage

between every one of these vehicles

and the total‑loss vehicle’s mileage

of 30,440 miles is at least five times

the legal limit of a difference of 4,000 miles

for substantially similar vehicles.

Accordingly, none of these vehicles

even come close to legally qualifying

as a substantially similar vehicle.

To arrive at a fair valuation,

you asked me to find comparable vehicles

within a 25 mile radius of my ZIP Code, 07722.

To be comparable,

otherwise substantially similar vehicles

would have to have odometer readings

between 26,440 miles and 34,440 miles.

However, just as CCC

was unable to find any vehicles

that meet these requirements

of the New Jersey Administrative Code,

I have been unable to find any such vehicles.

As I understand the sections

of the New Jersey Administrative Code

that govern auto physical damage claims,

the New Jersey Department of Banking

And Insurance allows insurers

to use valuation methods other than

relying on vendors such as CCC.

I would think that using an alternative method

would be especially advisable

when none

of a valuation services vendor’s comp vehicles qualify as substantially similar

to a claimant’s total-loss vehicle.

One alternative methodology

that NJ Administrative Code 11:3-10.4

Adjustment of total losses (a)(1.)(iii) provides

is retail values from these manuals:

“Manuals approved for use

on or after January 1, 1976 are

“Automobile Red Book” and

“Older Car/Truck Red Book” published by

Maclean Hunter Market Reports, Inc.

and the “N.A.D.A. Official Used Car Guide”

and “N.A.D.A. Official Older Car Guide”

published by the National Automobile Dealers

Used Car Guide Company.”

As I’m sure you know,

the New Jersey Administrative Code also says,

“If the insurer elects to make a cash settlement,

it must bear in mind at all times

that the insured’s position

is that of a retail consumer

and the settlement value arrived at

must be reasonable and fair for a person

in that position.”

That is, the required settlement value is

the retail value necessary to replace

the total‑loss vehicle.

I obtained a retail value for the total‑loss vehicle

from the online version of one of these,

the N.A.D.A., at

https://www.nadaguides.com/Cars/2018/Mazda/Mazda3/Wagon-5D-Grand-Touring/Values .

The N.A.D.A. retail value is $21,625.

A copy of the valuation report accompanies

this letter.

As is not the case with CCC’s

deeply flawed valuation, I would accept

the N.A.D.A. retail value as a fair, legal

and legitimate actual cash value.

This alternative, approved valuation

methodology leaves us with:

$21,625 Actual cash value

+ 1,433 Sales tax @ 6.625%

= $23,058 Cash value plus sales tax

$23,058 Cash value plus sales tax

- 500 Deductible

= $22,558 Claim settlement

Given the absence of substantially similar

vehicles that have mileages within 4,000 miles

of the mileage of the total‑loss vehicle

and that are for sale within twenty‑five miles

of the total‑loss vehicle’s ZIP Code

of garagement, I hope that you

and your colleagues will agree

that the N.A.D.A. retail value

is a value that is fair to all.

Thank you again for all of your gracious

assistance.

With best personal regards,

Maria

After Maria sent the letter,

we were thinking,

“Maybe they’ll come back

with an offer to meet her half way.”

Maria was thinking,

“If they offer to meet me half way,

I’ll probably accept that offer.”

Less than a week after Maria emailed

the letter to her insurance company,

she got an email back from them.

Here’s what the insurance company’s

response to Maria’s letter said:

Good Afternoon Maria,

I reviewed the additional paperwork you

supplied and in efforts to resolve the claim,

I can use the NADA Guides value you

supplied.

I can offer you a settlement as follows:

$21,625.00 NADA Guides value

+ 1,432.66 tax

--------------------

= 23,057.66

- 500.00 deductible

--------------------

= $22,557.66

Please confirm you agree/accept

and I will reach out to your lien holder

to obtain pay off information.

I look forward to hearing from you.

Thank you and have a great day!

REDACTED

When Maria and I read the email,

we both yelled the same reaction:

“ W h o a ! ! ! ”

The insurance company

didn’t meet Maria half way.

They met her all the way!

High fives! Yes! Maria rules!

Maria! Maria! Maria!

What did Maria achieve?

When Maria pointed out

the omissions and errors

in the CCC market valuation report’s

description of her total‑loss vehicle,

she got a $450 or 3% increase

in CCC’s pre‑sales‑tax

valuation of her vehicle.

When Maria pointed out

the flaws

in how CCC valued her total‑loss vehicle

and proposed using the NADA Guides valuation instead,

she got an additional $3,708

or 21% additional dollars

in the insurance company’s valuation

of her total‑loss vehicle.

In sum, sales tax included,

Maria increased the valuation

of her total‑loss vehicle

from $18,624 to $23,058.

That’s $4,434 additional dollars!

That’s 24% additional dollars!

That’s $4,434 additional dollars

just for writing one email

and then one letter.

The hours of work

that Maria did

to get a fair valuation

paid off handsomely.

Total-loss claimants

who live in New Jersey

have a right of recourse.

Should Maria have exercised

her right of recourse?

Perhaps.

Perhaps not.

Maria’s claim was a first-party claim.

She was dealing with

her own automobile insurance company.

Maria chose not to exercise

her right of recourse

because she had had

her automobile insurance

and her homeowner’s insurance

with the same insurance company

for decades.

Maria reasoned that,

if she pressed her insurance company

to the max

on the valuation

of her total-loss vehicle,

then, at some future date,

her insurance company

might be less than fully cooperative

on a bigger, more complicated claim

under her homeowner’s coverage.

If Maria had been able to find

a substantially similar vehicle

for sale at an automobile dealership

and she had exercised her right of recourse,

Maria likely could have gotten

even more money.

But, often in life, we have to balance

what we want to gain in a transaction

against what we want to preserve

in a relationship.

Maria struck the balance

that she believed

was best for her.

Even if your total-loss claim

is a first-party claim

in which you are dealing with

your own automobile insurance company,

your situation may be different.

Your reasoning may be different.

You may be able to find

a substantially similar vehicle

for sale at an automobile dealership

that is for sale at a higher price

than your total-loss vehicle’s

J.D. Power Buy from Dealer price.

You may want to get

all the money you can.

You may want to exercise

your right of recourse.

If your total-loss claim is a third-party claim

in which you are dealing with

the automobile insurance company

of an at-fault driver

whose negligent act

caused the destruction of your vehicle

and you have a right of recourse,

then you have no reason not to exercise

your right of recourse

if doing so is likely to get you

more money.

Whether you agree

with Maria’s decision or not,

Maria broke trail.

Maria helped pioneer

wasyourcartotaledorstolen.com.

Through her example,

Maria is showing you

and millions of other Americans

how you and they

can get fair valuations

of your total-loss vehicles

in first-party total-loss claims.

If you achieve more than Maria achieved,

you will do so, in part,

because Maria did what she did

and beause she gave me permission

to share what she did

with you.

Thank you, Maria!

You are an inspiration to us all!

What_Maria_did_to_get_her_more_moneyChapter

What I did to get

thousands of more dollars

for my total-loss vehicle

than the valuation amount

in the CCC market valuation report.

A little after 6:00 AM one Sunday morning,

while I was home asleep,

a young woman,

who had been out drinking all night,

while she was driving

on the street where I live,

passed out at the wheel.

She crashed the 2008 Toyota

that she was driving

into my vintage 1986 Jeep Cherokee.

My parked Cherokee kept her car

from crashing

into a thirty‑foot‑tall sycamore tree—

impact with which might have killed her.

Other than drunk,

the young woman was okay.

Her Toyota was totaled.

My Cherokee was totaled.

The young woman’s negligent act

(driving while drunk, passing out,

and crashing into my vehicle)

caused the destruction of my vehicle.

Travelers was the insurer of her vehicle.

Hence, my total-loss claim

was a third-party claim

against the negligent at-fault driver

and Travelers.

A few days after the crash,

a Travelers Claim Appraiser

inspected my vehicle.

Based on his inspection,

at Travelers’s request,

CCC Information Services

a.k.a. CCC Intelligent Solutions

prepared a CCC market valuation report

for my vehicle.

The Claim Appraiser emailed me

a copy of that document.

The CCC market valuation report

valued my total‑loss vehicle at $1,644.01

(which included the New York City

vehicular sales tax at 8.87%).

I was surprised at how low

the valuation was.

Why was it so low?

When I looked at the details

of the CCC market valuation report

for my total-loss vehicle,

I discovered that the description

of my vehicle contained lots

of omissions, errors, and misrepresentations.

If I let Travelers and CCC get away

with these omissions and errors,

I would not get a fair valuation

of my total‑loss vehicle.

Accordingly, I wrote the following letter

(which I have redacted slightly)

to the Travelers Claim Handler

who was handling my claim.

Re: Claim H3H9516

CCC Market Valuation Report

Dear Ms. REDACTED,

Early Sunday morning, August 21,

your insured party Jacklyn REDACTED who,

according to the police report, was driving drunk

(aggravated driving while intoxicated),

crashed into and totaled my Jeep Cherokee

that was parked on Bleecker Street

near my residence in New York, NY.

At the request

of Travelers Claim Appraiser Vladimir Titensky,

CCC prepared a Market Valuation Report

for my Jeep Cherokee.

Mr. Titensky provided me

with a copy of that report.

I was appalled, disappointed and mystified

to discover that the Market Valuation Report

that CCC prepared is filled

with inaccurate statements,

sloppy representations and misrepresentations

that— were I to rely on them—

could prove to be fraudulent misrepresentations.

In the table on the following pages,

I itemize page by page

the report’s obvious inaccuracies, sloppiness,

and potentially fraudulent misrepresentations.

The question I have for you is this:

Does Travelers intend to pursue settlement

of my claim on the basis of CCC’s inaccurate,

sloppy and potentially fraudulent report?

Or will Travelers undertake an accurate,

careful and honest valuation of my vehicle

that Ms. REDACTED is charged

with the crime—

among others—

of destroying?

More generally, I cannot help but wonder:

For its valuation reports, will Travelers continue

to do business with and rely upon a company—

CCC— that produces inaccurate, sloppy

and fraudulent reports?

CCC’s Representations

Problems with CCC’s

Representations

“Loss vehicle has 2% greater than average mileage of 183,900.”

CCC does not bother to mention

what it is that they average

so they can calculate

a greater‑than or less‑than

percentage of average mileage.

One might assume that the relevant average

would be the average mileage of vehicles

of the same age and category type.

According to the U.S. Department of Energy’s

report of Average Annual VMT

[vehicle miles traveled] per Vehicle

by Vehicle Type available at http: //www.afdc.energy.gov/uploads/data/data_source/10308/10308_fuel_use_veh_type.xlsx,

light‑duty vehicles are driven

an average of 11,346 miles per year.

Hence, the average mileage

of a 30‑year old light‑duty vehicle

would be roughly 340,380 miles.

Hence, the vehicle that CCC purports to value

has not 2% greater than average mileage

of 183,900 but 45% less than average mileage

of 340,380.

BASE VEHICLE VALUE

This is derived from comparable vehicle(s)

available or recently available

in the marketplace at the time of valuation,

per our valuation methodology described

on the next page.”

The vehicles that CCC used

as comparable vehicles

were not available or recently available

in the marketplace

at the time of valuation.

CCC telephoned two dealers

who had no comparable vehicle

in their inventories and asked them,

if they had such a vehicle,

what would they sell it for.

SEARCH FOR COMPARABLES

When a valuation is created

the database is searched

and comparable vehicles

in the area are selected.

The ZIP Code where the loss vehicle

is garaged determines the starting point

for the search. Comparable vehicles

are similar to the loss vehicle

based on relevant factors.”

Comparable vehicles in the area

were not selected. CCC identified

no comparable vehicles in the area.

Comparable vehicles were not similar

to the loss vehicle based on relevant factors.

The “comparable vehicles” that CCC used

did not and do not exist.

“Finally, the Base Vehicle Value is

the weighted average of the adjusted values

of the comparable vehicles

based on the following factors:

· Source of the data

( such as inspected versus advertised)”

The source of the “data”

for comparable vehicles that CCC conjured up

was neither inspected nor advertised.

It was conjecture.

VEHICLE ALLOWANCES

Odometer 186,713 - $30

Presumably, the $30 deduction

from the value of the vehicle

for its odometer reading is because,

in CCC’s analysis,

the vehicle has “2% greater

than average mileage of 183, 900.”

In fact, the vehicle has 45% less mileage

than average vehicles of the same type and age.

Hence, instead of taking a $30 deduction

because of the mileage, CCC should add $675

to the value of the vehicle.

“These allowances are displayed

for illustrative purposes only.”

CCC makes a big to‑do

about its quantitative and data‑driven methodology. Yet, in this caveat,

it claims that its numbers are meaningless.

WTF?

“Transmission 4 Speed”

The transmission is 5‑speed manual

with overdrive.

“Seats: Clean.

Appear to be recently replaced.”

Seats are original. Their like‑new condition reflects the gentle use that this vehicle got.

“Headliner: No significant scuffing.”

Headliner was recently replaced.

At time of crash, it was immaculate.

“Paint: Numerous large deep chips and scratches. Heavy peeling, flaking, fading. Significant fading.”

Paint had no large deep chips.

It had no peeling or flaking.

It had minimal fading.

The paint did have some tiny scratches

from leaning a bicycle against the left rear side.

“Glass: Stone damages

and crack on the windshield.

Scratches and heavily pitted.

Numerous chips.”

Windshield had small, repaired crack

below wiper area on driver’s side.

Windshield had one BB‑size chip

near inside rearview mirror.

Windshield was not heavily pitted.

It did not have numerous chips.

“Engine: Numerous old and new leaks.

Belts and hoses worn.”

Engine had neither old nor new leaks.

Belts and hoses were recently replaced.

“Transmission: Numerous leaks evident.”

Transmission did not leak.

List Price

Comp 1 $2,000

Comp 2 $1,500

“List Price is the sticker price

of an inspected dealer vehicle

and the advertised price

for the advertised vehicle.”

Loss Vehicle Odometer 186,713

Comp 1 Odometer 186,713

Comp 2 Odometer 186,713

That the prices that CCC gives as List Prices

for their Comp 1 and Comp 2 vehicles

are not list prices is obvious res ipsa loquitur

(Latin for “the thing speaks for itself”)

from the loss vehicle’s odometer reading

and the two comp vehicles’ alleged

odometer readings. The odds

of three randomly selected, 30‑year‑old vehicles

having exactly the same odometer readings are

astronomical— perhaps 1 in 100 trillion or so.

Comp 1

1986 American Motors Cherokee 4wd

6 2.8l Gasoline

Dealership B & L Auto

Contact Mohammad, Stephan

Telephone (718) 652-2277

Source Dealer Quotation

Stock # NA

Obtained Date: 08/25/2016

Distance from New York, NY

12 Miles - Bronx, NY

I spoke by phone with Mr. Stephan Mohammad

on Friday, August 26, 2016.

Mr. Mohammad said he had no Jeep Cherokees

in stock nor had he recently had any.

He said that valuation companies ask him

what he might sell a particular vehicle for

if he had one.

In no manner is any price Mr. Mohammad

may have given CCC a list price—

“the sticker price of an inspected dealer vehicle

and the advertised price

for the advertised vehicle.”

Comp 2

1986 American Motors Cherokee 4wd

6 2.8l Gasoline

Dealership Gold Automart

Contact (owner), Aboud

Telephone (973) 507-9919

Source Dealer Quotation

Stock # NA

Obtained Date: 08/26/2016

Distance from New York, NY

20 Miles - East Hanover, NJ

I spoke by phone with Mr. Aboud Dawli

on Monday, August 29, 2016. Mr. Dawli said

he had no Jeep Cherokees in stock

nor had he recently had any.

In no manner is any price Mr. Dawli

may have given CCC a list price—

“the sticker price of an inspected dealer vehicle

and the advertised price

for the advertised vehicle.”

The valuation report also omits

at least one addition to the loss vehicle

that increased its value: a few weeks ago,

I replaced the car’s useless cigarette lighter

with a USB port that has both 1‑amp

and 2.1‑amp ports.

When Ms. REDACTED crashed into my car,

the impact burst out the right rear window

and crumpled the car

so that the passenger‑side door

could not be closed completely.

To keep rain water from getting

inside the car and into its electrical system,

the day of the crash, a Sunday,

I bought plastic sheeting and tape

and covered the right side of the car.

I would like to be reimbursed for that $25.02:

H BRICKMAN & SONS NEW YORK NY;

Transaction date: 08/21/2016;

Transaction type: Purchases;

Merchant description: HARDWARE STORES;

Merchant information: NEW YORK, NY;

$25.02.

While Travelers Claim Appraiser

Vladimir Titensky seems like a nice man,

he did not inspect my vehicle

with the professionalism

that I expected from a Travelers employee.

Instead of allowing me to participate

in the inspection with him and, thereby,

resolve differences of observation,

Mr. Titensky asked me to stand

next to his illegally parked car

and make sure that he did not get

a parking ticket.

Protecting Mr. Titensky from parking tickets

was not the reason

for which I made myself available

on the day scheduled for the inspection.

I could have made more valuable use of my time

elsewhere.

I hope that CCC’s inaccurate, sloppy

and potentially fraudulent valuation report

is an anomaly for Travelers

and that Travelers has as its basic goal

the prompt and fair settlement of all claims—

mine included.

I look forward to working with you

to achieve a fair settlement of my claim.

Thank you.

With best personal regards,

Gerald L. Marlow

In response to my letter,

a Travelers representative phoned me.

He was senior to the Claim Handler

with whom I had spoken theretofore.

(Perhaps the company culture at Travelers

is such that they let a charming woman

handle a claim until they discover

that the claimant is not an idiot?

Then they turn the claim over

to a combative prick?)

This Travelers’s representative said

that they do not have to use

CCC’s valuation.

They have other ways

that they can value total‑loss vehicles.

While I was on the phone,

the Travelers’s rep

quickly came up

with an alternative valuation.

He increased Travelers’s settlement offer

from $1,644 to $1,804.60,

a 10% increase of $161.

Travelers sent me a settlement check

for $1,804.60.

I did not know it at the time,

but, in my subsequent research,

I learned, apropos the Travelers’s rep’s

quickie, on‑the‑phone valuation,

that New York State law says the following:

The insurer shall provide

to the insured,

no later than the date

of payment of the claim,

a detailed copy of its calculation

of the insured vehicle’s total loss value,

including the valuation of options

which are not considered

in the base price of the vehicle.

N.Y. Comp. Codes R. & Regs. tit. 11 § 216.7

Did the Travelers rep,

as the law requires, provide me

with a “detailed copy of [his] calculation

of the insured vehicle’s total loss value?”

What?

Obey the law?

Did that notion

ever even cross

the rep’s Travelers‑trained mind?

I dunno.

What do you think?

I was unhappy

with the quickie low valuation.

I smelled misconduct;

but, at the time,

I knew next to nothing

about how insurance companies

are supposed to settle total‑loss claims.

Hell, up until my ordeal with Travelers,

I was so naïve that I thought

insurance companies were honest.

I deposited the check.

I researched the New York State laws

that govern how insurance companies

must settle total‑loss claims

in the State of New York.

I learned that,

if an insurance company’s valuation

of a claimant’s total‑loss vehicle

is not enough money

for the claimant to buy

within twenty‑five miles of his or her home

a replacement vehicle

that is substantially similar

to his or her total‑loss vehicle,

then the law gives the claimant

a right of recourse.

If a person exercises

his or her right of recourse,

then New York State law requires

the insurance company

to do one of three things:

-

Value the claimant’s vehicle

at enough money to buy

a substantially similar vehicle

that the insurance company found; or, -

Pay the claimant the difference

between the amount

of its initialclaim payment

and the cost

of a substantially similar vehicle

located by the claimant;

or the insurer,

upon consent of the claimant,

may purchase that vehicle for the claimant; or, -

Value the claimant’s vehicle

on the basis of a price quotation

for a substantially similar vehicle,

obtained by the insurer

from a qualified dealer

located within 25 miles

of where the claimant usually garaged

his or her total-loss vehicle.

I exercised my right of recourse.

To do so, I sent Travelers

the following letter:

Mr. Adam J. Guillaume

Travelers Insurance

60 Lakefront Boulevard

Buffalo, NY 14202

Re: Claim H3H9516 recourse demands

as provided for under New York law

Dear Mr. Guillaume,

I hereby exercise my right of recourse under

211 NYCRR 216;

OFFICIAL COMPILATION of CODES, RULES AND REGULATIONS of The STATE of NEW YORK;

TITLE 11.

INSURANCE DEPARTMENT;

CHAPTER IX.

UNFAIR TRADE PRACTICES;

PART 216.

UNFAIR CLAIMS SETTLEMENT PRACTICES AND CLAIM COST CONTROL MEASURES.

Early Sunday morning, August 21, 2016,

your insured party Jacklyn REDACTED who,

according to the police report, was driving drunk

(aggravated driving while intoxicated),

crashed into and totaled my Jeep Cherokee

which was parked on Bleecker Street

near my residence in New York, NY.

On September 17, 2016,

as initial payment of my claim

for total‑loss of my vehicle,

I received from Travelers a check for $1,804.60

($1,657.50 + $147.10 tax).

For this amount of money,

I cannot purchase a vehicle

comparable to my total‑loss vehicle.

Accordingly, as the recourse provisions

of New York State Insurance

codes, rules and regulations require of Travelers;

I hereby demand that Travelers:

-

Reopen my claim, Claim H3H9516.

-

Identify a vehicle substantially similar

to my total‑loss vehicle

available from a qualified dealer

located within 25 miles of

3 Washington Square Village;

New York, NY 10012. -

Pay me the difference between

the amount of your claim payment to date

and the cost plus tax

of the substantially similar vehicle

that Travelers identifies. -

To compensate me

for loss of use of my vehicle,

provide me with a rental car

of the same class as my total‑loss vehicle

until this claim is closed.

To assist Travelers in identifying

a substantially similar vehicle,

I enclose a copy of the window sticker

from the total‑loss vehicle.

I base these four demands

on the following requirements

found in 211 NYCRR 216.

General

Section 216.10 Standards for prompt,

fair and equitable settlement

of third‑party property damage claims

arising under motor vehicle

liability insurance contracts.

This section is applicable to claims arising

under motor vehicle liability insurance contracts

affording coverage for claims

of property damage by third parties caused

by the alleged negligence of the insured.

The following provisions of this Part

shall also be applicable to these claims:

sections

216.0(a), (b), (d), (e);

216.1;

216.2(preamble);

216.3;

216.4(b), (c), (d), (e);

216.5;

216.6(a), (b), (e)‑ (g);

216.7(a), (b)(4)‑ (6), (11)‑ (13)(c)(1), (3), (4); and

216.11.

Section 216.7 (c) (4) Right of recourse.

If, within 35 calendar days

after mailing of the claim payment,

the insured notifies the insurer in writing

that the insured cannot purchase

a comparable vehicle for the market value,

as determined under the provisions

of subparagraph (1)(i), (ii), (iii) or (v)

or paragraph (3) of this subdivision,

the insurer shall reopen its claim file

and shall offer, in its discretion

and subject to applicable deductions,

one of the following options to the insured:

Section 216.7 (c) (4) (i)

the insurer shall identify and offer for settlement

an amount sufficient to purchase

a substantially similar vehicle,

as provided in subparagraph (1)(ii)

of this subdivision; or

Section 216.7 (c) (4) (ii)

the insurer shall pay the insured

the difference

between the amount of its claim payment

and the cost of a substantially similar vehicle,

as provided in subparagraph (1)(ii)

of this subdivision, located by the insured,

or the insurer, upon consent of the insured,

may purchase that vehicle for the insured.

Section 216.7 (c) (1) (ii)

A quotation for a substantially similar vehicle,

obtained by the insurer from a qualified dealer

located reasonably convenient to the insured.

A reasonable location shall be within 25 miles

of the place of principal garagement

of the motor vehicle.

The substantially similar available vehicle

must remain available for purchase

by the insured

for a period of three calendar days

subsequent to receipt of notice of its availability

by the insured, and

the insured must be able to purchase

the substantially similar vehicle

at the quoted dealer for the insurer’s cash offer

plus applicable deductions.

The insurer must maintain in its claim file

the dealer’s name and location,

the vehicle identification number,

the dealer stock number, the mileage

and the major options

for the substantially similar vehicle

which was the basis of its quote.

The notice to the insured of the availability

of a substantially similar vehicle

must be sent by certified mail,

return receipt requested,

or be a sound‑recorded conversation

reflecting the date of notice.

The three calendar days commence

on the date the insured acknowledges

receipt of notice.

The insured need not purchase the vehicle

used as the basis of the insurer’s quotation,

since the quotation merely serves as a basis

for the insurer’s offer.

The foregoing period is satisfied at the point

an insured physically verifies the existence

of the substantially similar available vehicle

used as the basis of the insurer’s quotation.

Should the insurer’s research

of substantially similar vehicles determine

that the retail values contained

in the valuation manuals,

prescribed in subparagraph (i) of this paragraph,

are inadequate

to purchase a substantially similar vehicle,

the insurer’s offer should be

the amount determined by such research.

Section 216.10 (a) (3) (i)

In all other claims, the written acknowledgement

by the insurer shall inform the claimant

that the insured has a policy which,

to the extent of the insured’s negligence,

provides coverage for property damage,

including the loss of use of damaged property

and any other out‑of‑pocket expenses

reasonably attributable to the accident.

As you are aware

from my September 5, 2016 letter to Travelers,

in its initial investigation of my claim,

Travelers made many misrepresentations—

many of which— if not all—

violated New York State law.

I trust that, henceforth,

Travelers will conform to the law’s requirements

and, in a timely manner,

fulfill the four demands

communicated in this letter.

I look forward to

Travelers’s prompt satisfaction

of the requirements of insurers

who do business in the State of New York.

Thank you.

With best personal regards,

(Signed) Gerald L. Marlow

From Travelers, I received this response:

Dear Mr. Marlow:

Please let this communication

serve as confirmation that we have received

your letter notifying us

that you are invoking your right of recourse.

Under the right of recourse

we were unable to locate

a substantially similar vehicle

as per subparagraph (4)(ii)

of the NYCRR 216.7.

If you have located a vehicle

which meets the criteria as outlined

please notify us immediately.

Sincerely,

Adam Guillaume

Claims Professional

There’s chicanery at work

in Adam’s response:

In my research, I learned that,

in some states,

the law says that the valuation

of a total‑loss vehicle

must be the retail price

of a substantially similar vehicle

or better

for sale at an automobile dealership.

While Travelers might not have been able

to find a substantially similar vehicle

(if they even looked),

they easily could have found

a similar‑but‑better vehicle

for sale at an automobile dealership

In response to Adam’s brushoff,

I made numerous phone calls to Travelers.

I urged them to comply with the law

and settle my claim accordingly.

(It was on one of these phone calls

that the Travelers rep

whom I imagined

to be a lavishly rewarded,

Waikiki‑bound beach boy asked,

“Did you deposit the check?”)

After I had made a few

of these fruitless phone calls,

I received this letter

from a higher up at Travelers:

Dear Mr. Marlow:

As follow up to my voice message

left for you on July 17th

allow this letter to confirm

that there is no appeal process

and our stance on value stands

as previously outlined.

If you have any additional questions

feel free to contact me directly.

Sincerely,

Chris Stavers

Unit Manager

In their interactions with the public,

representatives of many corporations

seem to believe

that they are the final arbiters of disputes.

They act accordingly.

But, in disputes,

corporate representatives

do not have the final say‑so!

In the United States of America,

courts are the final arbiters of disputes.

To the degree that arbitrators, judges,

and juries are impartial;

plaintiffs and defendants

appear before the court on equal footing.

No matter how pompous and arrogant

a corporate executive may be,

an impartial arbitrator, judge, or jury

treats the parties before the court

without fear or favor.

I decided to sue Travelers

in New York County Small Claims Court.

(New York County

is what New York State

calls Manhattan.)

First, I searched online for a vehicle

that was substantially similar

to my totaled, two‑door,

1986 Jeep Cherokee

with manual transmission—

one that was for sale

at an automobile dealership.

Golly gee, you know?

Two‑door, 1986 Jeep Cherokees

with manual transmissions

are hard to find!

They are so hard to find

that the closest to such a vehicle

that I could find was a twelve‑years‑newer 1998 four‑door

with manual transmission

for sale sixty‑six miles away.

Travelers and CCC initially valued

my 1986 Jeep Cherokee at $1,644

(sales tax included).

This 1998 four‑door Jeep Cherokee

was for sale for $5,982 (sales tax included).

Said I to myself,

“I really would prefer a two‑door!

But, since this one sells for almost four times

what Travelers and CCC

valued my totaled vehicle at,

I guess that, for valuation purposes,

I can make do with this one

as an acceptable substitute vehicle.”

As one of my claims against Travelers,

I would ask the Court to order Travelers

to pay me the difference

between the $5,982 cost

of the acceptable substitute vehicle

and the $1,804 initial‑settlement check

that Travelers sent me.

That difference was $4,178.

$5,982

- $1,804

= $4,178

At the time, the maximum amount

for a judgement award

by a New York County Small Claims Court

was $5,000. (Now it is $10,000.)

I went to the Office of the Clerk

of the New York County Small Claims Court.

I filled out the one‑page form

to initiate my lawsuit.

I paid the $20 court fee.

The Clerk gave me a court date.

I was in and out of the Clerk’s office

in twenty minutes.

When you file a lawsuit,

you make one or more claims.

Your arbitrator, judge, or jury

considers each of your claims separately.

In my lawsuit, I was making three claims.

The arbitrator or judge for my lawsuit

could decide in my favor

for none of my claims,

for one of my claims,

for two of my claims,

or for all three claims.

After I filed my lawsuit,

in Microsoft Word,

I wrote up my claims

and the award amount

that I sought for each claim.

For each claim, I cited the New York laws

on which I based my claim.

I printed the Word document.

I printed CCC’s valuation reports.

I printed my letters to Travelers

and their responses.

From my online bank account,

I printed a copy

of the initial settlement check

that Travelers sent me.

I printed the sales advertisement

for the acceptable comp vehicle

that I had found.

I organized these printed pages

into one master document.

To the master document,

I added the police accident report.

To the master document,

I added the invoice for the rental car

that Travelers provided me with

at their expense

when my claim was opened the first time—

immediately after the destruction

of my vehicle.

At trial, you’re supposed

to give the court

and give your adversaries

copies of any evidence

that you’re presenting at trial.

I took my master document

to my local photocopy shop.

I had the photocopy shop make

several copies of the master document

and bind each copy in a comb binding.

(If you sue the insurance company,

ask the clerk of your court

if you should bind pages of evidence

or leave them unbound

for presentation at court.)

When my court date rolled around,

I chose to have my case heard

by an arbitrator instead of by a judge.

Neither Travelers nor the drunk driver

bothered to show up.

In New York (and in most other states),

when you sue someone

in Small Claims Court

and that party does not show up for the trial,

you do not automatically win.

What would have been a trial

becomes an inquest.

You still have to convince

the arbitrator or judge

that you deserve

to win the amount of money

for which you are suing.

Over the course of a little less than an hour,

I explained to the arbitrator

what happened.

I explained to him my three claims

and the award amounts

that I sought for each one:

-

To reimburse me

for out‑of‑pocket expenses

that I incurred in connection

with the destruction of my automobile,

I asked for $25. -

To make up the difference between

the amount at which Travelers

had valued my total‑loss vehicle

and the retail price

of the twelve‑years‑newer vehicle

that I had located

and that I found acceptable,

I asked for $4,178. -

When I exercised my right of recourse,

that action re‑opened my claim.

As I understood the law,

Travelers was obligated

to compensate me for loss of use

of my total‑loss vehicle

while my claim was open (or re‑opened).In between the day

that I exercised my right of recourse

and the day that I filed my lawsuit,

728 days elapsed.To compensate me for loss of use

of my vehicle over those 728 days,

I asked for $51,043.

How did I arrive at $51,043?

When, immediately after the collision,

I opened my claim,

Travelers, at its expense,

provided me with a rental car

through Enterprise auto rental.

I kept the rental car until I received

the initial settlement check from Travelers.

Enterprise charged Travelers

$70.11 per day.

$70.11 per day X 728 days = $51,043.

The three claims totaled $55,246.

I gave the arbitrator one of the bound copies

of my claims, documents, exhibits,

and calculations.

I answered the arbitrator’s questions.

At the end of our conversation,

the arbitrator handed me a blank envelope.

He told me to write my name and address

on it.

I did so.

I handed the envelope back to him.

“Did you have to pay for the stamp?”

No, I did not have to pay for the stamp.

It was included in the $20 filing fee.

In parting, the arbitrator said to me,

“If you ever get tired of being a writer,

you should think about becoming

an attorney.”

A few days later, I opened my mailbox.

I saw the envelope

that I had addressed to myself.

I opened it.

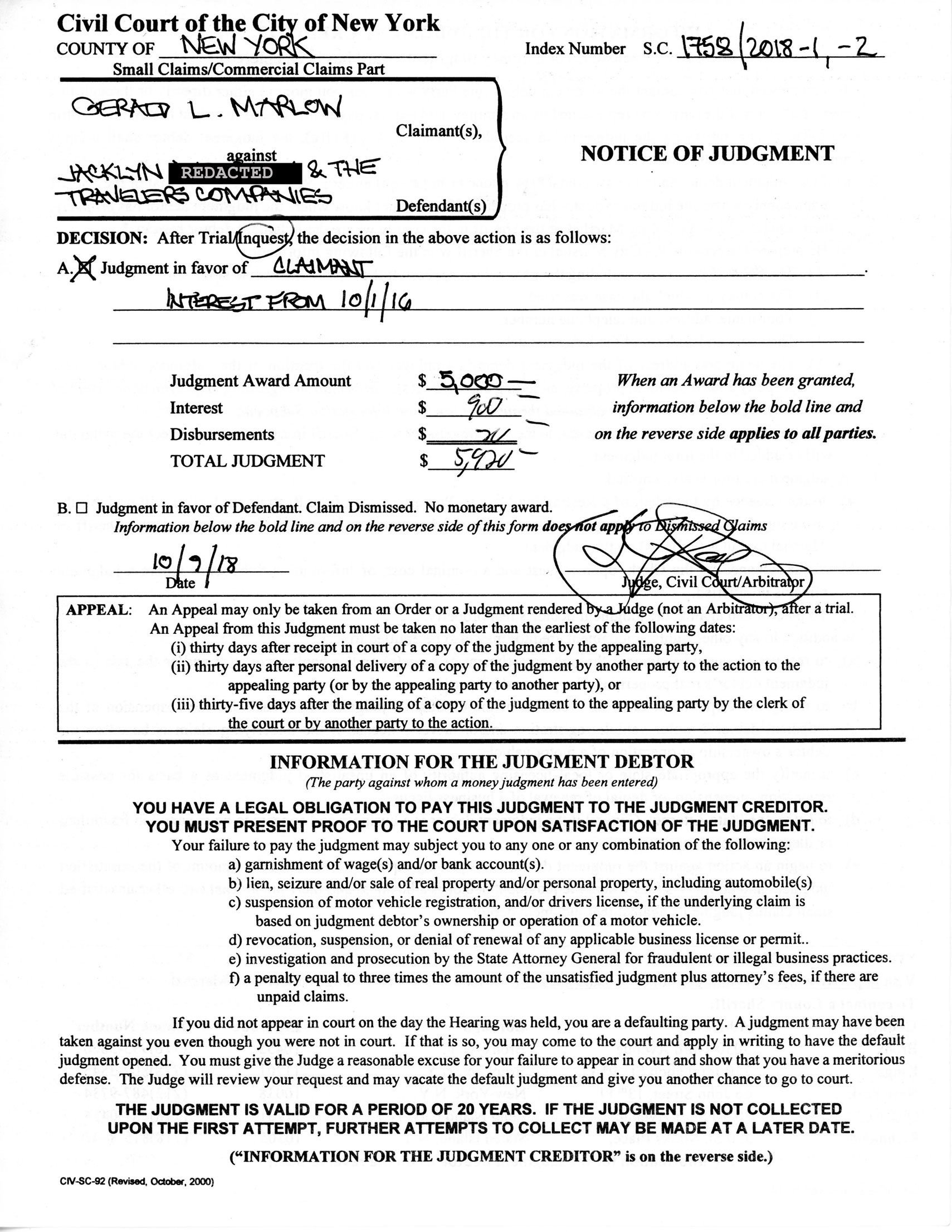

The arbitrator awarded me a judgement

against Travelers for $5,920.

That was the Small Claims Court’s

then maximum award of $5,000,

plus $900 interest,

plus reimbursement at Travelers’s expense

of the $20 court fee that I paid to sue them.

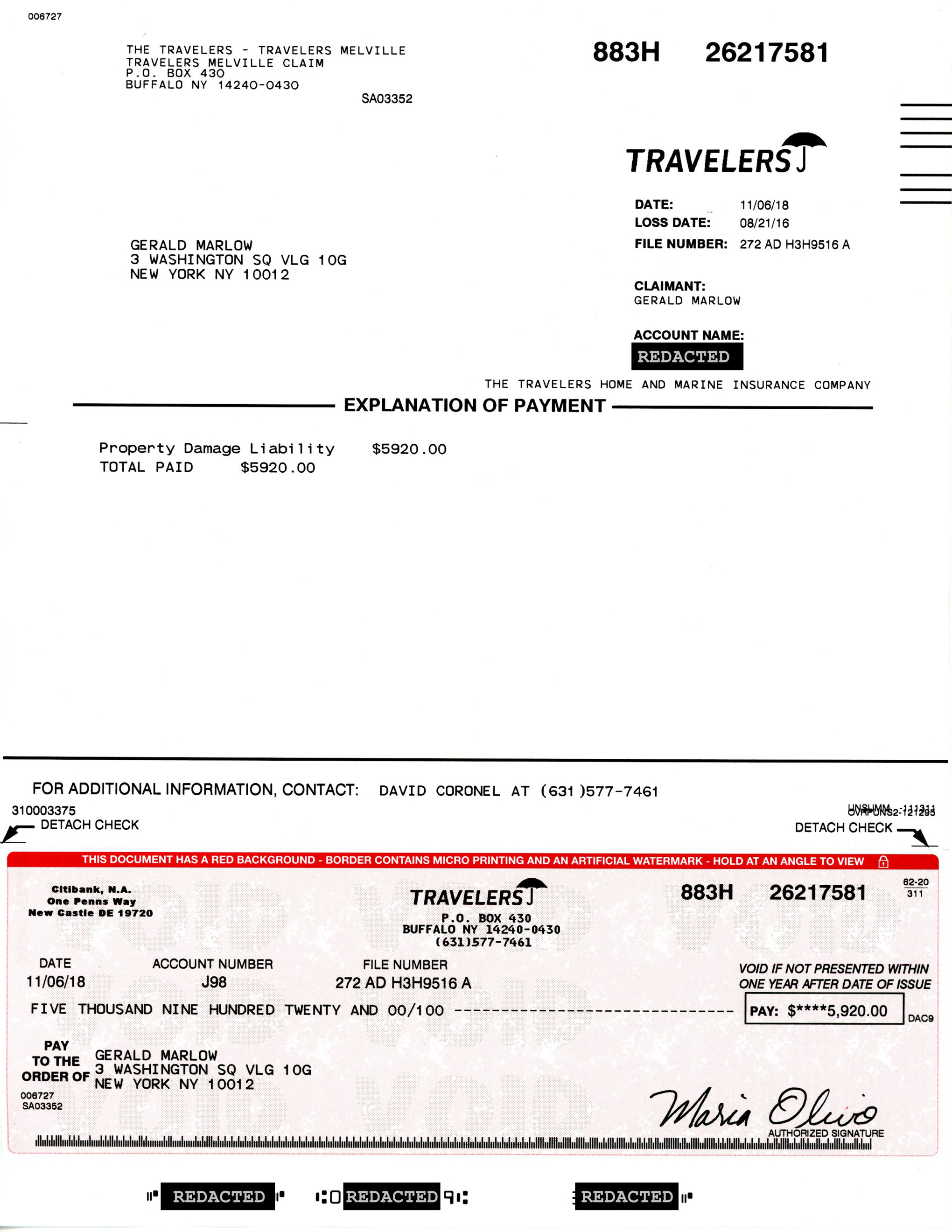

A couple of weeks later,

I received an envelope from Travelers.

I opened it.

The $5,920 was on top

of the initial settlement check

that Travelers sent to me for $1,805.

In sum, after I exercised the rights

that New York State law gave me

and then sued Travelers

in Small Claims Court,

I got a total of $7,725.

That’s $6,081 more

than the $1,644

at which Travelers and CCC

initially and bogusly valued

my total‑loss vehicle.

That’s more than four times

the amount of money

that Travelers initially offered me.

That’s almost $8,000 cash money

for a total‑loss vehicle

that Travelers

and CCC Information Services

a.k.a. CCC Intelligent Solutions

initially valued at well less than $2,000.

In the end, CCC’s misconduct

and Travelers’s arrogance and defiance

worked in my favor:

I got a lot more money

than I would have gotten

had they offered me a fair valuation

in the beginning.

Why didn’t Travelers show up in court?

I dunno.

Maybe they knew they were going to lose?

Maybe their standard operating procedure

is to try to screw all claimants

and then, whenever those efforts fail,

skip the court appearance?

Maybe Travelers regarded the then

small-claims maximum award

of $5,000

as chump change

and not worth their bother?

Beats me.

What’s your guess?

What_I_didChapter

What I would do today

to get a fair valuation

of my total-loss vehicle

improves upon

what Maria and I did

to get fair valuations

of our total-loss vehicles.

What I would do today

to get a fair valuation

of my total-loss vehicle

is a further evolution

of what Maria did

and of what I did

to get thousands of more dollars

for our total-loss vehicles.

The steps that I would take today

would incorporate

what I have learned

and what I have figured out

since I began developing

wasyourcartotaledorstolen.com.

Soon I will tell you

what I would do today

to get a fair valuation

of my total-loss vehicle.

I will tell you

what I would do today

if I had not yet settled

my total-loss claim.

I will tell you

what I would do today

if I had already settled

my total-loss claim

and I had a right of recourse

and my right of recourse

had not yet expired.

I will tell you

what I would do today

if the automobile insurance company

sent me a check for my total-loss vehicle

a year or more ago

but I never agreed in writing

to their valuation amount

and the statute of limitations

had not yet expired on my right to sue

the automobile insurance company

for the money

that they cheated me out of.

But first, let’s talk about your rights.

Let’s talk about the rights

that you have in the settlement

of a first-party total-loss claim.

Let’s talk about the rights

that you have in the settlement

of a third-party total-loss claim.

Let’s talk

about how and why

those rights are different.

The more you know about your rights,

the more confidently and adeptly

you will be able to navigate

the settlement of your total-loss claim.

Up_next_know_your_rightsChapter

Nota bene

Jerry Marlow is not an attorney. Neither information nor opinions published on this site constitute legal advice. This site is not a lawyer referral service. No attorney‑client or confidential relationship is or will be formed by use of this site. Any attorney listings on this site are paid attorney advertising. In some states, the information on this website may be considered a lawyer referral service.

Terms of use

Jerry Marlow grants human users of wasyourcartotaledorstolen.com permission to use the copyrighted materials on wasyourcartotaledorstolen.com for their personal use free of charge.

The fee to use copyrighted materials on wasyourcartotaledorstolen.com to train artificial intelligence software (AI) is $4 million.

Reproduction of copyrighted materials on wasyourcartotaledorstolen.com for commercial use without the written permission of Jerry Marlow is strictly prohibited.

Jerry Marlow does not grant users permission to reproduce on other websites any of the copyrighted material published on wasyourcartotaledorstolen.com.

Jerry Marlow does not grant users permission to reproduce via audio, video, or any other audiovisual medium any of the copyrighted material published on wasyourcartotaledorstolen.com.

If you wish to use any of the copyrighted material published on wasyourcartotaledorstolen.com in any way for which permission is not explicitly granted, contact Jerry Marlow at jerrymarlow@jerrymarlow.com.